What is a Recession?

How we talk about the economy when the economy is in uncharted territory

I saw a chart yesterday about the labor market and thought distinctly, “It doesn’t matter if we are in a recession or not, damage is done.” It made me wonder about the power that the word “recession” has. It brought together a few strands of thoughts that have been running through my mind.

What is a recession and are we in one right now? I have a long answer for you.

The Chart

The Declaration

The Words

The Story

1 The Chart

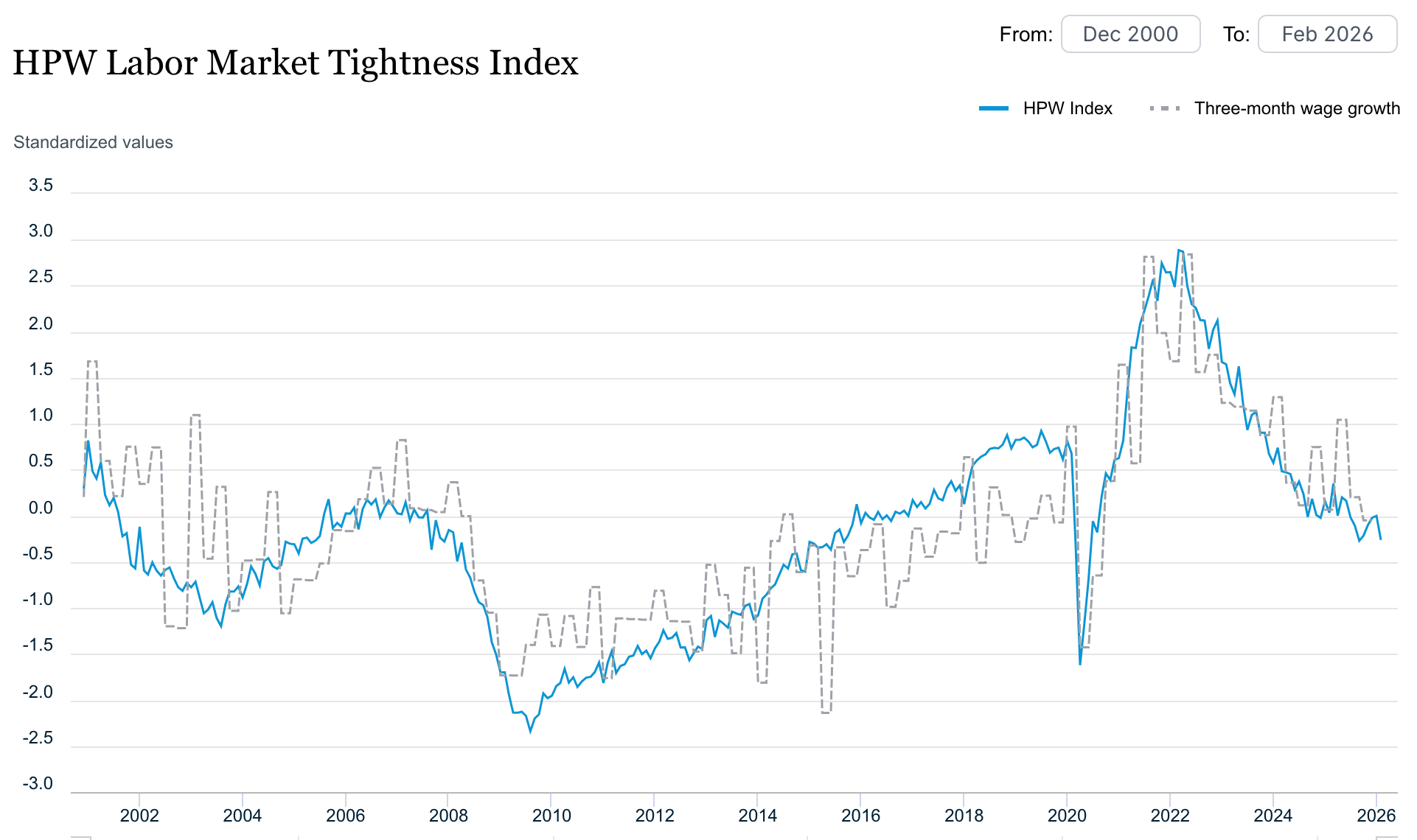

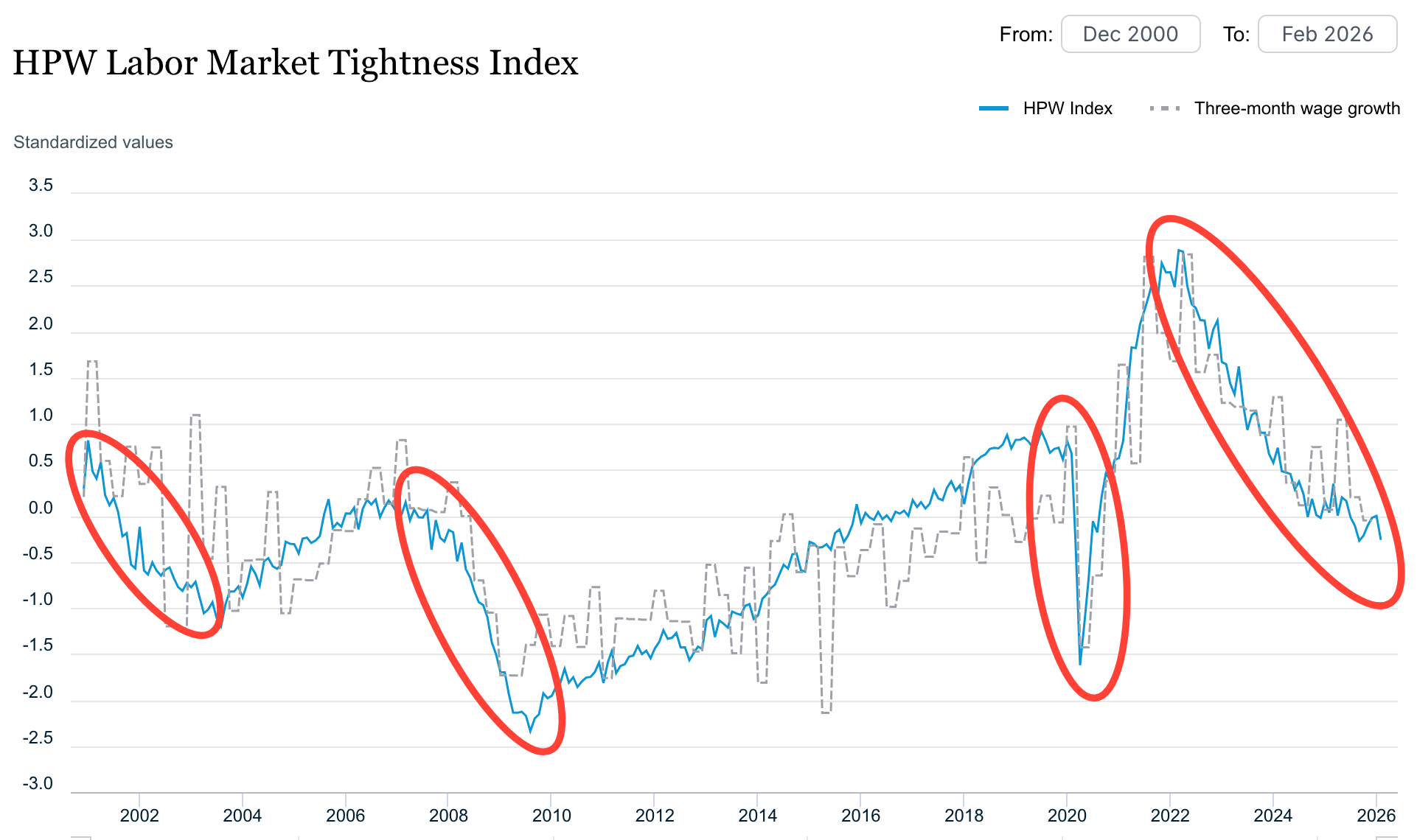

Here’s the chart that caught my eye. It’s called the HPW Labor Market Tightness Index (HPW is an acronym of the authors who came up with it, Heise, Pearce, and Weber). In the labor market, tight is good and loose is bad. You can think of it like: the economy can only be as big as the number of workers in it, like a beach ball can only be as big as its plastic casing. The labor market is tight when the ball is taut—we can’t blow much more air into it. The labor market is loose when the ball is slack—it needs more air.

Typically we measure tightness through the unemployment rate, which counts the share of workers who don’t have a job. The HPW Tightness (which does sound like a ship!) looks at unemployment relative to 1) how many people are quitting and 2) how many job openings there are. If a labor market is tight, there should be lots of movement of people leaving and moving jobs.

Here’s HPW Tightness since 2000, in blue. They also put three-month wage growth next to it, in gray.

Y’all, this chart is chilling.

It starts in 2000 and immediately falls—that’s the 2001 recession.

Then it rises and drops quickly again—that’s the 2007 aka great recession.

Then it slowly rises for a long time and has a sharp drop down and spike up—that’s the pandemic recession.

Then it rises again before falling for a long time—that’s 2022 to today.

I was struck by just how much the shape of the line over the last three years looks like the recessions that came before it. If anything it’s worse because it’s longer.

The reason why we are not officially in a recession is because however bad the current decline, the level of tightness is still good. HPW Tightness is right around 0 today—a level typically seen when the labor market is at its strongest just before a recession starts.

So that’s not good. Not only have we not put name to whatever misery the past three years have been, unless that line changes direction soon, it’s about at the level where all the prior recessions have started. We could be in a recession already.

How could we be in a recession and not know it?

2 The Declaration

The US has a cyclical economy. That means that it goes through ‘business cycles,’ a period bookended by recessions. It goes like this:

The economy expands

It stops a little bit and slows down (PEAK)

It hits a low (TROUGH)

It speeds back up and passes the point where it slowed down (RECOVERY)

The economy expands again (EXPANSION)

Or in econspeak:

Peak—>Trough—>Recovery—>Expansion—>Peak—>Trough—>Recovery—>Expansion—>Peak—>Trough—>Recovery—>Expansion—>Peak—>Trough—>Recovery—>Expansion—>Peak—>Trough—>Recovery—>Expansion—> you get it.

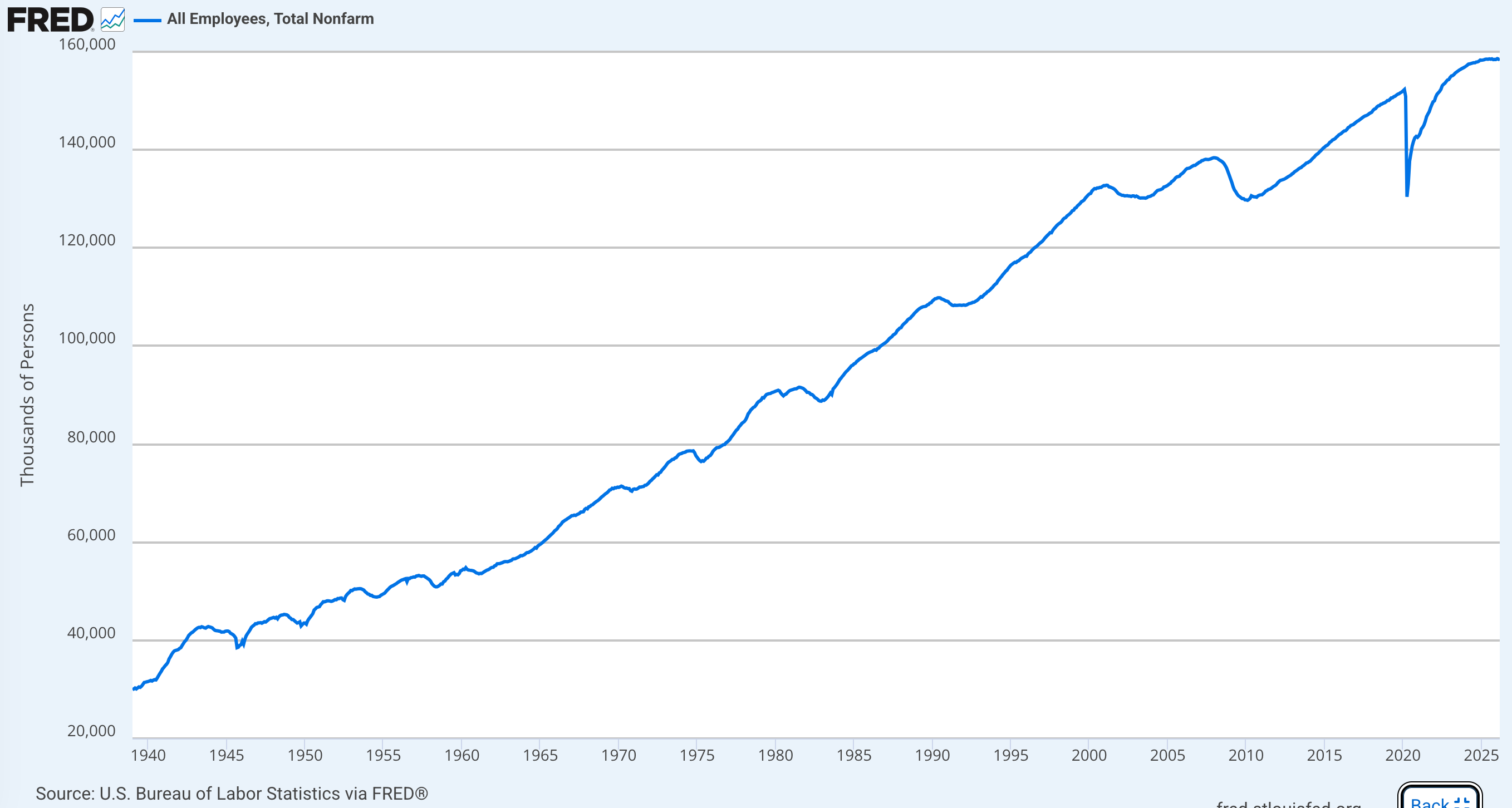

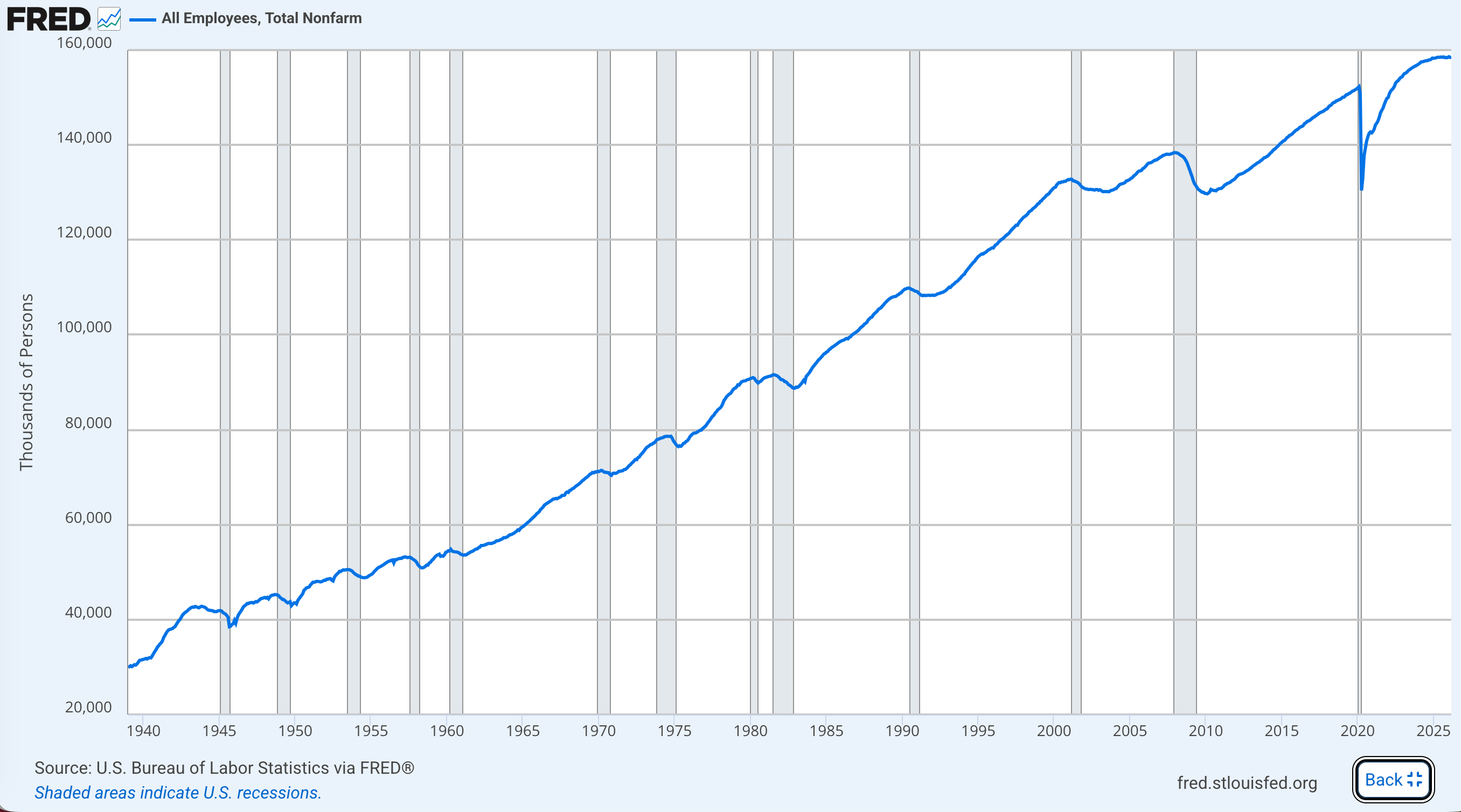

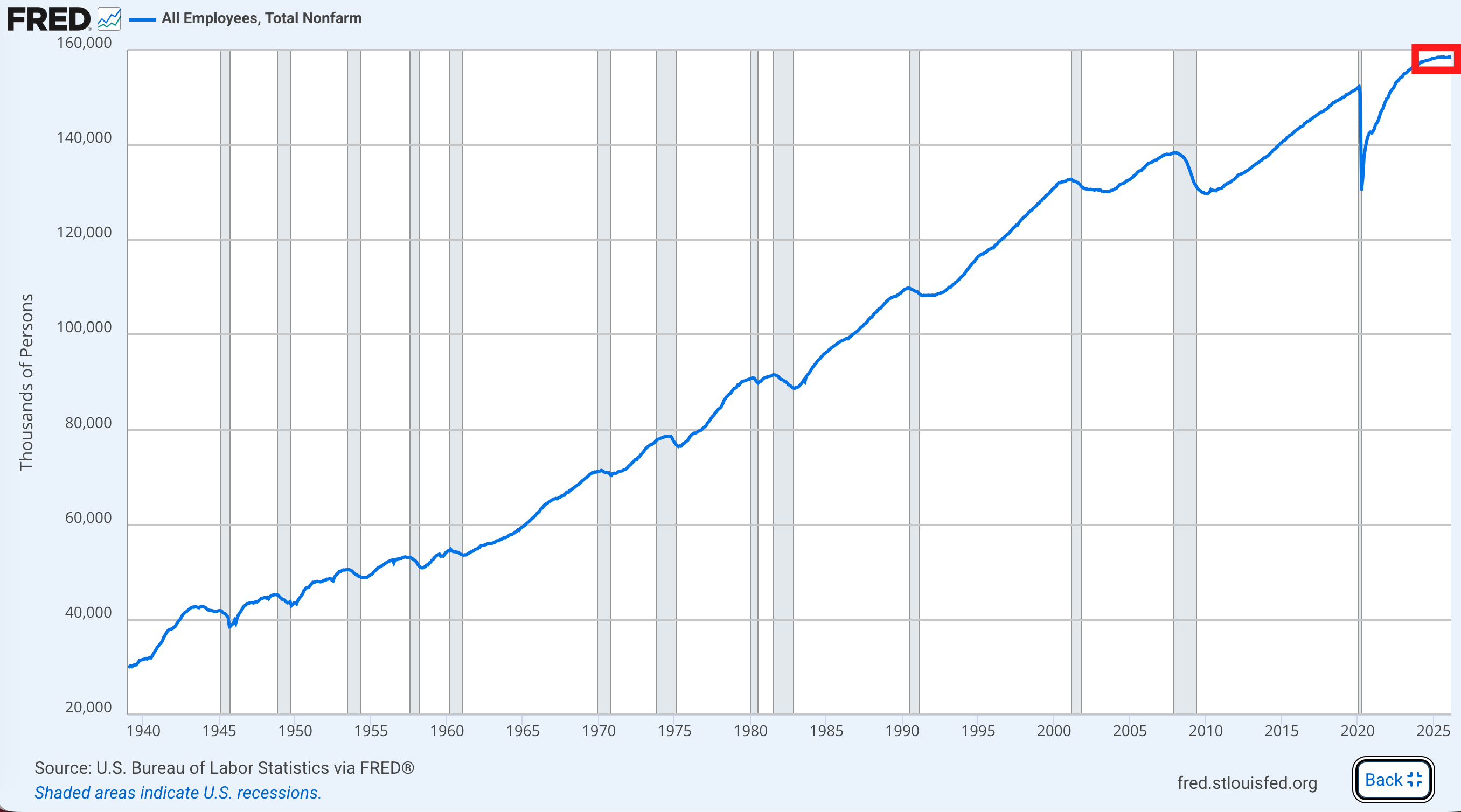

If you look at the total number of jobs in the economy, you can see the cycle visually. The economy is adding jobs i.e. the line is going up. Every so often there’s a divot aka recession, and then more jobs. You can also see how absolutely brutal the Great Recession was in 2007-2009 and how absolutely severe the 2020 pandemic shock was.

When do we know the economy is in recession? When is peak and trough? Believe it or not, there’s no official government agency that does this. It’s not like the Treasury Department issues a recession announcement, or the Federal Reserve, or any public official. It comes from a group of economists.

A private professional association (the National Bureau of Economic Research) has a group (the Business Cycle Dating Committee) that keeps a history of all recessions in the US and announces when a recession has begun and ended. They did this initially for research purposes back in the 1920s to set the record straight on when recessions happened to improve how they are studied. You can’t learn how a recession affects unemployment if researchers are using four different definitions of a recession.

Here’s the same figure, with the periods of official recession shaded in.

In modern times, the NBER announcement carries the weight of officialdom. Their definition is that a recession is:

“a significant decline in economic activity that is spread across the economy and that lasts more than a few months.”

You’ve probably heard the shorthand that a recession is two quarters of negative growth, but they’re careful not to make a rule out of it. Instead, they backdate recessions, announcing in, say, October that a recession started ten months early in December.

When you think about it, this is pretty incredible. When the economy shows signs of weakness, they wait to see how the story shakes out. Did the jobs report stay bad? Did inflation get better? Was GDP worse than we thought? And once the weakness is palpable enough to be a recession, they go back and say “Well, it all started here.”

So think of it as: when do you know when you’ve had a bad week? Surely not Monday afternoon. You could have had a horrible morning, but there’s a lot of week left to write it off entirely. Good things can still happen. But by Friday, when every day offered up some fresh awfulness, you can call it: this was a bad week. You’ve decided at the end that the week was bad the whole time. How we declare recessions is similar.

Why do it this way? Two reasons.

Don’t freak people out. A lot of the economy is moved by mood. Simply declaring a recession has started will worsen the economy to some degree, as people grow fearful and cautious and change their behavior. We wouldn’t want a recession to be too easy to declare because they carry their own momentum.

Get it together. Backdating a recession’s start gives policymakers room to maneuver. So say there’s a bad data report; we want policymakers to get to work to counter the weakness, look for problems, calm worries. Not every bad report should be a recession.

The US is not currently in recession. But we could have started one and will find out later. And there’s no rule, it’s not like the backdating of a recession start has some cap of, “oh we only go back three months, or ten months, or 15 months.” So long as the economy has signs of weakness, it’s up for recession grabs.

3 The Words

To review:

Labor market tightness is in decline in a way that looks like a recession or at least well on its way.

But it’s not a recession because not enough bad things have happened in the economy for one to be declared.

However you, person on the ground living your life, are struggling right now, please allow me, economist from my lofty perch, to tell you it’s not actually a recession.

Two stories for you.

Slam Poetry Inflation

At the end of 2023, I was at an elementary school in DC for a holiday concert, where each grade’s kids sang songs and did a dance. The program kicked off with a performance of the 5th grade slam poetry team. I stood there, in awe, as they performed a piece called “inflation.”

Believe it or not, inflation to these 10-year old kids was not about the monthly or yearly growth rate of prices in the economy. They talked about their mom pulling food out of the shopping cart at the grocery store, not being allowed to turn the heat up, how the 99 cent can of tea costs three dollars, all of it because of inflation. This word was a way for them to convey their economic struggles.

I wrote about it in a column, “The People’s Inflation Is Still a Big Problem,” and I explained how the statistical event of elevated inflation rates gave Americans a language to talk about issues far beyond the annual growth rate in prices.

At the time, I felt like because their use of the word was technically incorrect, a lot of Americans were being ignored, like: People who are complaining about inflation are wrong because inflation has fallen. But they weren’t talking about inflation inflation, they were talking about their inflation. Maybe they were failing a strict econ vocab test, but they weren’t wrong.

Econ 101

At the start of 2025 I was asked to give a lecture to a group of undergraduates who were going to spend the semester studying and working in DC. Since we had a newly elected president, I gave them a short history of the financial products that lead to the financial crisis and Great Recession to explain how current presidents are often credited or blamed for economic stories long in the making.

One of the students came up to me afterwards and said, “If what you said is so interesting, why is Econ 101 so awful?”

I agree with him, it’s pretty awful. The economy is of natural interest to anyone living in it. How much you earn, what kind of job you have, what you can buy, why your city has money or doesn’t—the economy determines so much.

And then you arrive bright-eyed, bushy-tailed in Econ 101, ready to learn about all these things that are part of your life, and instead you’re hit with a brick wall: two lines crossing on a graph. One is supply, one is demand, they meet at price. Somehow everything that you feel and like as a person can be expressed as a “preference curve” and your choices boiled down to “maximizing utility.” How that relates back to the real world is an opaque mystery, one you certainly don’t get to by the end of the semester.

What I told the student was: think of economics as a language.

Economists love to think of themselves as scientists, the physicists of human interaction. So they present Econ 101 like Physics 101: here are the most basic rules. The problem is that the economics rules are built in a world that has never, and will never, exist. Physics is accurate from day one—force always equals mass times acceleration. But economics feels inaccurate from day one—the market is never perfectly competitive, people never have a budget constraint limited to choosing between two (optional) goods, workers are never paid their marginal productivity. Why learn rules derived from a world we’ll never live in?

As a science, economics can feel like a sham.

So think of it as a language, closer to Spanish 101. No one arrives into an intro language class expecting to speak or talk like a fluent person would. There’s an artificial feel to every 101 conversation: the rigid formal speaking, the simple grammar, the selection of words that eschew the many exceptions to the rules of conjugation.

“Hello sir, where is the library?”

“The library is next to the dormitory.”

“Thank you.”

“You are welcome.”

Fluent speakers don’t sound like 101 learners, but you’ve got to get through 101 to become fluent.

I didn’t just say this to get the kid to stick with 101, I genuinely believe economics is like its own language. It’s not a wild take. In an academic department, it’s pretty common to call work outside of academic publishing as “translation.” So getting an article in a peer-reviewed journal is “research” and writing about that article in an op-ed or making a video about that article is “translation.” It’s an admission that we have our own way of speaking. Our language is part of how we parse the world.

Lost in Translation

Economists’ tightly held definitions—like inflation and recession—carry immense weight. That kid who performed a poem about inflation—he was taking over a word not just to convey his story, but also to give his story importance. People care about inflation, even if they don’t care about him and his mom struggling. He was rejecting the idea that inflation was over, not because he didn’t understand inflation, but because he understood it perfectly: it’s a time when important, powerful people cared that Americans couldn’t afford things.

I honestly don’t think economists have the words to talk about what we are going through in the labor market right now because we’ve never seen it before. Go back to the payroll chart I put above, with all the recessions. Typically, the economy is adding adding adding jobs, and then it falls. That’s easy to see. But right now, we aren’t adding or losing much. We’ve flatlined. That’s never happened.

In fact, if you go back through the jobs reports over the past ten months, the US has lost jobs in every other month: June, August, October, December, February. The annual growth in jobs in 2025 was 0.1%. That’s about as close to flat an economy this size will get. It’s like a lost year, a lost year that came on the heels of two weak ones.

We have held back calling this flatline a recession, and with it, held back the weight and seriousness that that word conveys. In a recession, Congress needs to do something. They need to help the unemployed, expand benefits, give money to states to keep services flowing. And in a recession, we get the acknowledgement that lasts throughout our worklife that we made it through a bad labor market, even if we still carry a lot of scars from it. No recession means no help and no recognition.

And it also means Americans are grappling with what is going on and are looking for a story that makes sense of all this.

4 The Story

The story they are jumping on is AI. We are growing without jobs because AI has taken them. It’s appealing. AI companies and AI proselytizers are certainly happy to fan the flames because it all creates a sense of urgency that everyone is using AI everywhere and if you haven’t then you’re behind. And given that AI investments are the only tailwind in the stockmarket right now, firms are eager to claim that they are using AI if only to keep their stock price up. The evidence that AI is replacing workers, however, is scant. It takes time for technology to be tested in the workplace, time for firms to adopt it fully, and time for that adoption to make workers obsolete.

The real story is longer and really is about the long tail of recovery from the pandemic and the economic problems it caused in the labor market and in prices. Here’s the tick tock:

2020: The pandemic craters the economy. More than 22 million jobs are lost in less than 5 weeks. By the end of the year, the US still posts 9.8 million fewer jobs. Consumer spending radically changes to accommodate new pandemic preferences and restrictions.

2021: The pandemic starts to end as vaccines become widely available and restrictions lift. The newly elected Biden administration passes a recovery package to keep the economy afloat and public services flowing. Jobs are recovered at a quick clip and consumer spending radically changes again. By the end of the year, inflation, which is considered okay so long as its under 2%, starts to jump up.

2022: The Fed, which has been waiting to raise interest rates because they were worried about jeopardizing the fragile labor market recovery, starts to raise them in March. In the summer, it’s extreme: the labor market is the tightest its ever been and inflation is the highest its been in 40 years. The Fed keeps aggressively raising rates, and both the labor market and inflation start to cool.

2023: There is widespread worry that a recession is coming. The Fed continues to raise rates through August, capping 18 months of increases. The labor market is weakening, inflation is weakening. The question is when it all bottoms out.

2024: Inflation continues to fall and the labor market continues to weaken. By the fall, price growth has fallen enough that the Fed lowers rates to stabilize the labor market. By the end of the year, four full years since inflation first started to increase, it seems over. Price growth is falling, on its way to 2%. The labor market is starting to put up big numbers for job growth. The economy is, we think, back to normal.

2025: The new administration pursues two contractionary policies and one inflationary policy. Firing federal workers and deporting unauthorized workers both hurt growth in the labor market. Increasing tariffs increases prices. All three policies lead to uncertainty among employers. The fallout is swift if not severe. The labor market loses jobs in 5 months of the year. Inflation still has not reached 2%. The Fed lowers rates a bit, but not enough to turn the weakness in the labor market around.

And here we are.

At some point, the economy will break in one direction or the other. But my mind keeps going back to the HPW Tightness chart, the decline that looks worse in shape than some of the recessions that came before it, and the people looking for a job right now. Declaring an official recession won’t change how they have struggled but how others see it, and the story we tell about it. It’s a failing of the economics language that that’s the case.

“I have a long answer for you”

Oh boy! *goes and makes a cup of tea*

Spectacular and important commentary on so many issues of relevance, in Kathryn's clear, singular voice. Sharing.