Tax Subcommittee Hearing on Your Paycheck, Returned

How the Working Families Tax Cuts Delivered for Americans

On Wednesday, I flew to DC to testify at the Tax Subcommittee of House Ways and Means about the One Big Beautiful Bill Act. Republicans have rebranded it the Working Families Tax Cuts Act, and if you knew nothing about it, you’d be forgiven for attending the hearing and assuming that the only provisions in the bill were ending taxes on tips and overtime, and that’s it.

It was a mean, mean room. I think the low point of the day, and surely a true low point in life, was when the Chairman of the full Ways and Means Committee attacked me for not being a real American. When I had a chance to speak next (you can only speak with their permission so he could say all this stuff to me and walk away), I passionately declared I was an American, without having to qualify myself.

I understand the cynicism. Why do this? Were they even listening? It’s all broken anyway so what’s the point?

The point is to try. I asked myself those same questions the first time I turned the phone around and started making videos for TikTok. I put out into the ether that our economy has problems that we can solve, and that Americans deserve to understand that. I don’t know who listens, I don’t know what lands, I don’t know what resonates, and I don’t know what changes minds.

So I don’t know if a Republican House member or their staff heard anything I said, just as I don’t know if you read to the end of this newsletter, or if anyone watches to the end of the videos. It’s such an obvious metaphor but it’s very fitting. You’re scattering seeds out into the dirt, seeing green shoots takes time.

Today’s edition of Kedits I wanted to share my testimony. Two days before the hearing, I submitted written testimony for the record. I’ve copied it here for you. Don’t feel like you have to read the whole thing! Really!

The testimony has to be no more than ten pages. I was generous with the font size, and even had a full page just for a summary and table of contents (it didn’t copy well to substack so it’s an image below). Even with that, it’s a lot. I’m making the case as succinctly and compactly as I can that the central ethos of Republican economic policy—that tax cuts are good for the economy—is wrong.

But like I said, the point is to try to put things out in the ether, even if it’s tax policy.

:D

You can watch my oral testimony here on TikTok. I also have it up on instagram.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

Testimony of Kathryn Anne Edwards, Ph.D. Economist

Summary

The purpose of the tax system is to raise revenue to fund government. With the release of the first quarter’s GDP estimate last month, the national debt exceeded the size of the economy. GDP was $31.22 trillion, and debt was $31.27. Outside of a brief period when the economy shrank precipitously in the pandemic, this has not happened since World War II. On average over the past fifty years, debt is about half of GDP.

Funding government has been usurped by economic aspirations and social objectives. The tax system is wielded liberally as a tool meant to fill in other purposes besides revenue. The results have been calamitous for the country’s finances and credit, which has been downgraded three times in a fifteen-year period. Even the solution—raise taxes—is similarly usurped by those economic aspirations and social objectives. The prospect of making the tax system do the job it is built to do is met with fear that it will cause too much pain.

In this testimony, I put forward that that fear is misplaced: tax policy is weak economic policy. The One Big Beautiful Bill Act is a fitting example of how tax policy is often deeply expensive and ultimately ineffectual. As a corollary, social purposes can be met as or more effectively through spending as through the tax code, but I spend less time on this point.

Note: I discuss only the tax provisions of the One Big Beautiful Bill Act, and not its spending components such as cuts to safety net programs or spending on immigration enforcement, both deleterious in their own way but less relevant to the tax system.

Key Point 1: Tax Policy is Weak Economic Policy

Tax policy in general is too sensitive to be reliably successful economic policy. Its potential economic effects depend on the macroeconomy at the time of enactment and how households behaviorally respond to a marginal change on a margin of their income. The former cannot be controlled, the latter cannot be predicted.

How a Tax Cut Could Grow the Economy

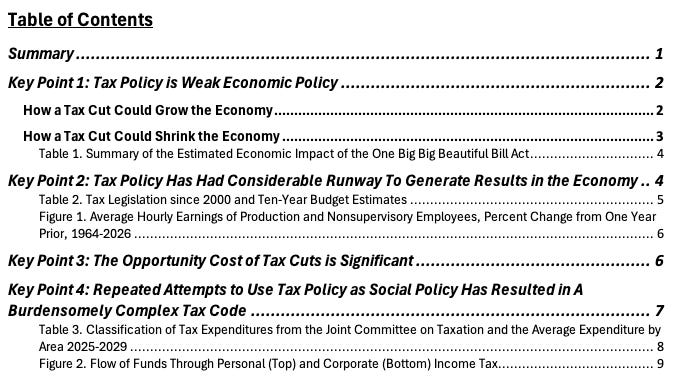

Consider the two primary channels of increasing economic growth over two time horizons: aggregate demand and aggregate supply in the short- and long-term. The four-square table below enumerates the macro conditions and behavioral response necessary.

The One Big Beautiful Bill Act failed to meet any condition.

- Short-term aggregate demand – There had not been a decline in aggregate demand (AKA gross domestic product minus net exports), so no boost was necessary.

- Short-term aggregate supply via work – The labor market was not very strong, the unemployment rate was in fact rising, and wage growth was falling; individuals could not find work so inducement to work more was ineffective.

- Short-term aggregate supply via savings – The tax cut was debt financed and households didn’t save it, as personal savings rate reached a post pandemic peak of 6.4 percent in January 2024 and has been declining since, reaching 3.6 percent in March of this year.

A short-term boost to aggregate demand has no long-term effect, and the long-term potential gains from boosting labor supply aren’t realized without any meaningful activity in the short-term.

Beyond a failure to meet basic conditions to be strong economic policy, the One Big Beautiful Bill Act has two separate problems.

The first is design. The overwhelming majority of the tax cuts in the One Big Beautiful Bill Act flowed to the richest households. In the bottom fifth of the income distribution, the net effect of the One Big Beautiful Bill Act was negative, according to the Congressional Budget Office, and under $400 for the next fifth. The top 10 percent, on the other hand, gained nearly $14,000 annually.[1] Money flowing to the richest households when the economy is growing does not do much to raise aggregate demand. To be fair, money flowing to the richest households could raise saving, with downstream effects on investment and growth, if that savings did not cost trillions of dollars in public debt, which the One Big Beautiful Bill Act did, and they actually saved it.

The second is monetary policy. In the year the One Big Beautiful Bill Act was passed, the Federal Reserve had interest rates at a relatively high level that they began to reduce. That suggests some minimum coherence between monetary and fiscal policy. But, by the end of 2025 and so far in 2026, rates have been held steady due to stubborn and now rising inflation, which was 3.8% last month. At the most recent Open Market Committee meeting, three members dissented from the language of the Committee’s statement on future rate cuts, wanting instead the Committee to commit to rate increases if prices continue to increase. In short, rate increases are on the table for 2026, which would negate the stimulative effects of a tax cut.[2]

For emphasis: If rates rise this year or next, the One Big Beautiful Bill Act tax cuts would be fueling demand as interest rates would be trying to dampen it, a remarkably unorganized and wasteful economic policy situation.

Finally, the One Big Beautiful Bill suffers from its historical timing. Tax policy has become chronically unstable. The behavior response of individuals to a change in after-time income—the response that drives broader economic effects—relies on individuals knowing that their after-tax income has increased and by how much. That is extremely difficult after of 9 major tax laws this century (not including recession-response tax policy) and numerous deductions and credits. It is plausible that most Americans have an imprecise idea of how much they pay or owe in taxes. That makes any tax policy, even one with perfect conditions, less effective.

This is not to say that the tax provisions of the One Big Beautiful Bill Act had no impact; it is pouring somewhere in the neighborhood of $450 billion into the economy. That leaves a mark. But effecting the economy and being an effective economic policy are not the same thing.

How a Tax Cut Could Shrink the Economy

Debt isn’t free; it incurs interest. And it has consequences, like decreasing the overall savings rate in the economy or bidding up the cost of borrowing. If a tax cut’s increase to public debt and borrowing is large enough, it can contract the economy in the long term.

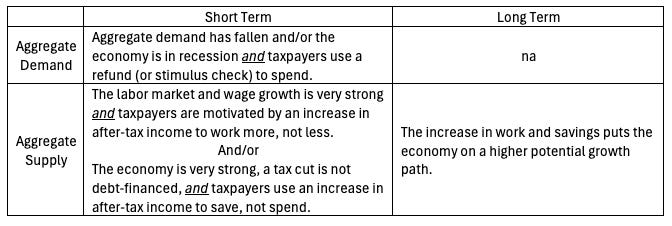

Estimates of the One Big Beautiful Bill Act’s economic impact came to that exact assessment. Table 1 summarizes economic projections from five budget and economic models. The economic impact of the One Big Beautiful Bill Act is frontloaded; the boost to GDP is largest in the first few years after enactment and then dissipates within a decade. Indeed, these estimates do not even have consensus that the One Big Beautiful Bill Act will have a positive impact by 2034. Penn-Wharton and the Yale Budget Lab find rather large decreases to the economy in the long run of 4.6% and 3.3%. Borrowing so much to pay for a tax cut now is akin to borrowing from future growth.

In Sum

The conditions necessary for tax cuts to be effective economic policy are difficult to meet, in general, and not met in the case of the One Big Beautiful Bill Act.

Key Point 2: Tax Policy Has Had Considerable Runway To Generate Results in the Economy

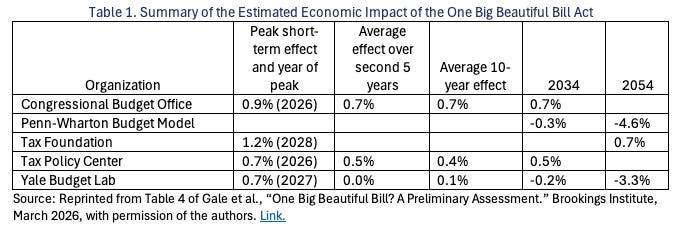

The One Big Beautiful Bill Act of 2025 is hardly our first rodeo when it comes to tax cuts. Since 2000, there are have been nine major tax actions (not including tax provisions related to recession response).[3] They are summarized in Table 2.

Combined these nine pieces of tax legislation represent a $13.1 trillion investment.[4] That investment was meant, as the names of the legislation indicate, to grow the economy, grow jobs, and help working Americans. Yet, it is hard to point to demonstrable and lasting success from this effort, hard to claim the economy has been inalterably transformed for the better or that it ushered in the most prosperous era yet.

Consider the basic measure of growth: the size of the economy, GDP. From 2001-2026, the economy grew at an average rate of 2.1%. The 25 years before that, it grew at 3.5% and the 25 years before that at 3.7%.[5]

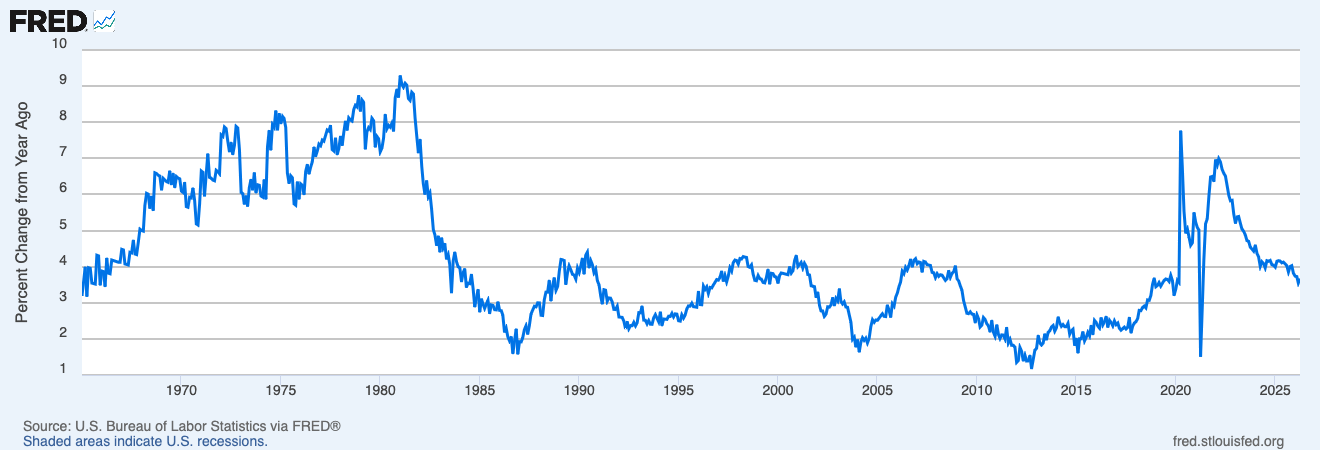

Similarly, if job growth had been robust, then the result would be fast wage growth—the more jobs, the lower the unemployment rate, the more employers have to compete for workers, and the more wages go up. Yet again, the era is disappointing. The average hourly earnings of production and nonsupervisory employees saw year-over-year nominal growth crater after the 1980 and 1981 recessions and did not recover growth above 5% for the next forty years. The pandemic labor market was the exception, and wages grew quickly in the summer of 2022, but fell again in the year after.[6]

Throughout this weak period for economic and wage growth, workers took home a smaller share of the pie. The share of gross domestic income that goes to the compensation of employees has been falling since 2000 and is below 52% from a peak of 58.4% in 1970. The last time workers took home such a small share was in 1941.[7]

These trends in growth, wages, and income have lots of determinants—changes in the population, concentration of businesses, trade, deep recessions, the strength of their recoveries—and tax cuts were no match for them.

Figure 1. Average Hourly Earnings of Production and Nonsupervisory Employees, Percent Change from One Year Prior, 1964-2026

In Sum

The US government has spent $13.1 trillion this century testing the ability of tax cuts to influence growth and prosperity. If they had worked well, it would not be so difficult to see their positive impact. The conclusion is that the economy poses challenges that tax cuts don’t solve.

Key Point 3: The Opportunity Cost of Tax Cuts is Significant

Even by federal standards, $4.5 trillion—the size of the tax cuts in the One Big Beautiful Bill Act—is a lot of money. If the One Big Beautiful Bill Act tax cuts were a spending program, they would be larger than all other programs aside from Medicaid, Medicare, and Social Security. For example, $4.5 trillion over ten years:

- Is half the size of Medicaid ($7.5 trillion).

- Is one-third the size of Medicare ($13.1 trillion)

- Is more than what Congress owes the Social Security trust fund ($2.8 trillion).[8]

- Is 4 times the size of the Supplemental Nutrition Assistance Program ($1.1 trillion).

But the greater cost to $4.5 trillion in reduced revenue is investment that could have been made with it, at a fraction of the costs. A report from the Brookings Institute estimates that the One Big Beautiful Bill Act’s tax portion was enough to cover the entire 75-year Social Security shortfall.[9]

Or consider, Congress could have passed a fully refundable Child Tax Credit ($1.6 trillion), created a universal paid family and medical leave program($228 billion), and created a universal preschool program with subsidized 0-to-3 child care ($381.5 billion)—for less than half the cost of the tax cuts in the One Big Beautiful Bill Act. [10]

And unlike tax cuts, these would be social programs have generated significant evidence to support the conclusion that they have an enormously beneficial effect they have on the economy. Poverty in children, inequality among children, and the high costs of raising children produce clear, deleterious consequences in our economy and society.

The one-year experiment with a fully refundable and expanded child tax credit in 2021 lifted 2.9 million children out of poverty, and resulted in the lowest child poverty rate on record.[11] A similarly modeled spending program could achieve the same results. Researchers estimate that the net social benefit would be ten times its cost through children’s higher future earnings and tax payments, improved health, and reduced cost in crime, health care, and child protection.[12]

Paid family and medical leave is a relatively cheap program. Its economic dividends have been studied most in the case of newborn care; they accrue from improvements in maternal and infant health and earnings of working mothers. Researchers estimate that the net social benefit would be 7-29 times its cost, depending on how leave is structured and its length.[13]

A basic income for children and paid leave program have weak effects on income and earnings of parents; their benefits accrue from making children less poor and healthier. Free child care, on the other hand, generates enormous earning returns. The expansion of one-year of free preschool in Connecticut, for example, increased the earnings of parents by 21% the year of preschool with higher income for another seven years after, generating $10 of return for every $1 spent through earnings of parents alone, not including beneficial effects on children’s education outcomes in the short and long term.[14]

Investing in children and families is not sensitive to macroeconomic conditions. It just works.

In Sum

The cost of the tax cuts in the One Big Beautiful Bill Act is equivalent to becoming the fourth largest spending program in the US federal pantheon. It is a lost opportunity to invest in programs that are cheaper and have proven net benefits to American families.

Key Point 4: Repeated Attempts to Use Tax Policy as Social Policy Has Resulted in A Burdensome Complex Tax Code

Tax expenditures—provisions in the tax code such as credits or deductions that reduce tax liability or increase tax refunds—have ballooned to $2.3 trillion a year. That is more than all other discretionary programs, more than the combined spending on health including Medicare and Medicaid, and larger than Social Security.[15]

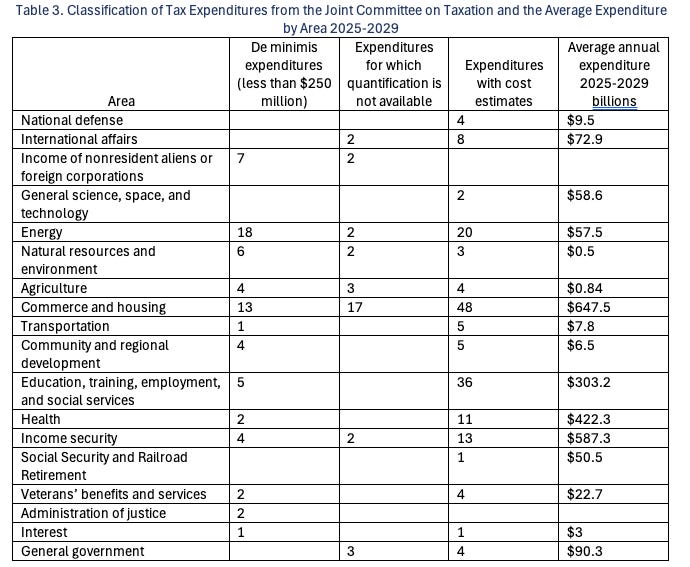

Tax expenditures are entitlements meant to subsidize some behavior or group through a reduction in taxes. The One Big Beautiful Bill created nine new ones. Table 3 summarizes the Joint Committee on Taxation’s report on expenditures—transcribing it and presenting it in a table.[16] The enumeration totals 271 separate tax expenditures.

The RAND Corporation has developed a tax analysis tool as part of its budget model. They have mapped how money flows through the tax system into visuals. The level of detail and intricacy is difficult to make readable in an 8x11 page, so I have copied the images here—as inscrutable as they are—because the complexity is conveyed if nothing else.[17]

As a result of this complexity, one of the fastest growing prices in the economy since 2000 is ‘tax preparation and accounting services.’ Cumulative growth in average annual prices from 2000 to 2025 was 87%. Over the same period, tax preparation and accounting services grew 204%. That is more than shelter (115%), fuel and utilities (141%), college tuition (188%), and day care and preschool (147%). It is shy of the hospital services’ 274%. According to Intuit Accountant, which sells tax preparation software to tax preparers, the average cost for an income tax return, from those who charge for preparation, ranges from $237 to $537.[18] It possible that there are Americans for whom the reduction in taxes is less than the increase in the cost to prepare them.

At the same time, there is no progress in developing Direct File, so that the IRS operates free tax filing for Americans. This despite the assessment of the Government Accountability Office that IRS’s Direct File was effective and had very high user satisfaction.[19]

Figure 2. Flow of Funds Through Personal (Top) and Corporate (Bottom) Income Tax

Many of these expenditures are worthy, valuable investments that produce desirable outcomes in the economy and society. But there is a cost of pushing them through the tax system. When it is instead wielded as a complex bonus mechanism, the job of raising revenue is overshadowed by the phalanx of constituencies who are rewarded by the tax expenditure and become advocates for keeping the tax system complex. That is not the failing of constituencies or their causes. Nor is it thus the conclusion that all tax expenditures are bad. But tax expenditure policy ought to be reviewed and right-sized so that only necessary (i.e. must be tax policy) expenditures are included.

In Sum

The complexity of the tax code undermines its ability to raise revenue and is expensive for taxpayers.

From Key Point One

[1] Congressional Budget Office. “Distributional Effects of Public Law 119-21,” 2025. Figure 1. Link.

[2] “Federal Reserve issues FOMC Statement,” April 29, 2026. Link.

From Key Point Two

[3] For more information, see Congressional Research Service RL34498, “Federal Individual Income Tax Brackets, Standard Deductions, and Personal Exemption: 1988-2026.” Link.

[4] Cost estimates for tax legislation can include offsetting non-tax measures, like spending cuts. The estimates here are ( intended to be) the tax portion only.

- The ten-year cost estimates for EGTRRA, JGTRRA, WFTRA, and TIPRA are summarized in Congressional Research Service R41134, “The Impact of Major Legislation on Budget Deficits: 2001 to 2009.” Link.

- TRUC, and ATRA come from Congressional Budget Office, “H.R. 4853, Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010,” and “H.R. 8, American Taxpayer Relief Act of 2012,” Link and Link.

-PATH from Joint Committee on Taxation, JCX-143-15, “Estimated Budget Effects of Division q of Amendment 2 to the Senate Amendment to HR 2029, the Protecting Americans from Tax Hikes Act of 2015.” Link

- TCJA and OBBBA come from Congressional Budget Office, “Appendix B: The Effect of the 2017 Tax Act on CBO’s Economic and Budget Projections, “Estimated Budgetary Effects of Public Law 119-21, to Provide for Reconciliation Pursuant to Title II of H. Con. Res. 14, Relative to CBO’s January 2025 Baseline.” Link and link.

[5] Bureau of Economic Analysis, via FRED series GDPC1

[6] Bureau of Labor Statistics, via FRED AHETPI

[7] Bureau of Economic Analysis, via FRED A4002E1A156NBEA

From Key Point Three

[8] “Actuarial Status of the Social Security Trust Funds.” Social Security Trustees. Link.

[9] Gale et al., “One Big Beautiful Bill? A Preliminary Assessment.” Brookings Institute, March 2026. Link.

[10] - Child Tax Credit:” Congressional Budget Office. “Re: Budgetary Effects of Making Specified Policies in the Build Back Better Act Permanent.” 2021. Link. This is the most generous and therefore most expensive version of the child tax credit, and a discussion of policy options can be found in “Factors Affecting the Cost of the Extending the Child Tax Credit.”IN11851 Congressional Research Service, 2022.

- Preschool and Child Care: Congressional Budget Office, 2021 “Economic Effects of Expanding Subsidized Child Care and Providing Universal Preschool.” Link.

- Paid Family Leave: Congressional Budget Office, 2019. “H.R. 1185 The FAMILY Act.” Link.

[11] Burns and Fox, “The Impact of the 2021 Expanded Child Tax Credit on Child Poverty.” Working Paper SEHSD-WP2022-24, United States Census Bureau, 2023. Link.

From Key Point Four

[12] Ananat and Garfinkel. “The Potential Long-Run Impact of a Permanently Expanded Child Tax Credit.” 2023, Annals of the American Academy of Political and Social Science.

[13] Wang et al. “The Benefits and Costs of Paid Parental Leave in the United States.” 2025, Social Service Review.

[14] Humphries et al, “Parents’ Earnings and the Return to Universal Pre-Kindergarten.” 2025 NBER Working Paper, 33038.

[15] ‘Tax Expenditure’ is the official term, defined in the Congressional Budget and Impoundment Control Act of 1974 as “revenue losses attributable to provisions of the Federal tax laws which allow a special exclusions, exemption, or deduction from gross income tax or which provide a special credit, a preferential rate of tax, or a deferral of tax liability.”

[16] Joint Committee on Taxation, JCX-45-25, “Estimates of Federal Tax Expenditures For Fiscal Years 2025-2029.” Link.

[17] Price et al. “Unlocking the Tax Code with RAND’s Tax Code Analysis Tool.” RAND Corporation, RB4392-1.

[18] Intuit Accountants Team, April 2026, “Practice Management: How Do Your Tax Prep Fees Stack Up?” link.

[19] Government Accountability Office 25-106933 “Direct File: IRS Successfully Piloted Online Tax Filing But Opportunities Exist to Expand Access.”

Yep, I know you’ve said this before and it’s been proven not to work by every Administration since Reagan that’s cut taxes. It doesn’t flipping work.

What we need to do is readjust the tax brackets, and if some billionaire uses their stock to secure loan, it gets taxed the value that it is being used to secure. I don’t care if you do or don’t sell it you’re utilizing it for a financial reason.

Corporate tax needs to get bumped up as well and honestly, if companies get to take away expenditures before they’re taxed, we should get to do it at home. All of our utilities, some portion of food up to a maximum, and maybe even our transportation cost should all be excluded before the taxes are calculated.

Thank you for that testimony you are most certainly an American.

I am a woman in Indianapolis, an RN, a mom, a wife, a gardener, a blue dot Hoosier— and I watch to the end of every one of your TikToks. I read to the end of each Substack you post. It infuriates me that they attacked you, but it’s no surprise. I am sorry that happened to you. They are deplorable. I appreciate your intelligence, humor, and hope. You help me understand the economy. I talk about your posts with family and friends, and I usually repost them. Keep going Katherine, I believe in you.